FEMA is No Substitute for Home Insurance

The stated mission of the Federal Emergency Management Agency (FEMA) is “Helping people before, during, and after disasters.” In partnership with state and local agencies and private organizations such as the American Red Cross, the Salvation Army, and many others, FEMA is tasked with helping people recover from disaster. However, the help they can provide is limited.

A FEMA employee, recently returned from extended field duty, spoke at length with the staff of Common Sense Eastern Shore. He assisted people whose homes were damaged by flooding (Hurricane Florence) and uprooted trees (Hurricane Michael) to apply for FEMA aid and shepherd them through the complex process of obtaining it. He detailed key limits of that assistance:

- Cash grants to repair home damages are only awarded to very-low-income people whose homes are underinsured or not insured at all. The maximum award is $34,900, regardless of the extent of the damage.

- Most assistance from FEMA is provided in the form of subsidized, low-interest loans up to $200,000, confusingly administered by the Small Business Administration.

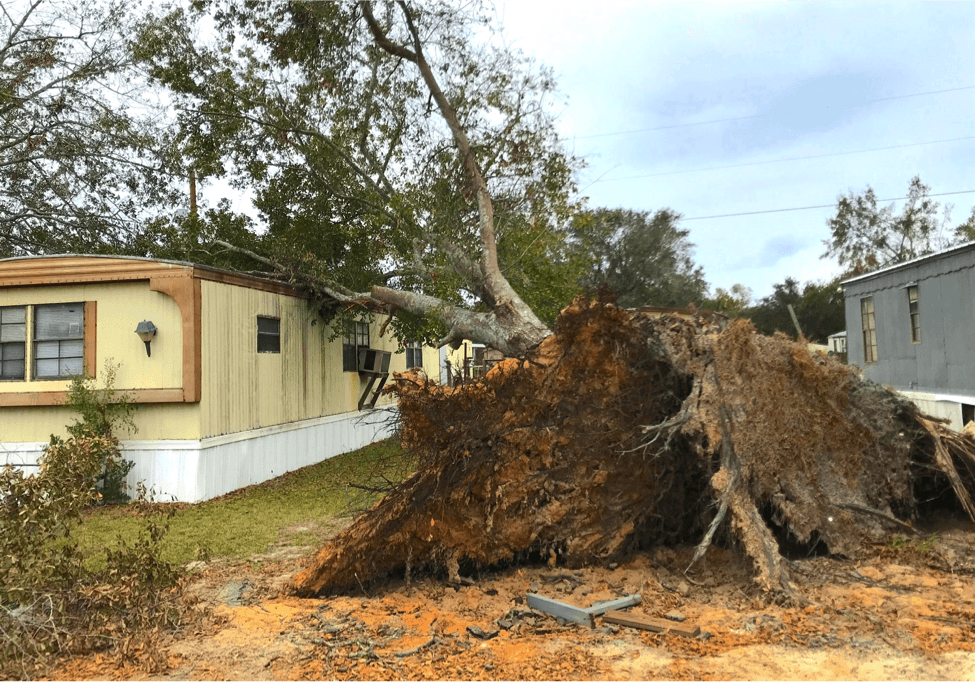

- The amount of a grant or loan is only enough to make the living area of a home “safe, sanitary, and functional”—not to fully restore a house or yard to its pre-disaster condition. FEMA does not help to fix sheds, porches, fences—or even spare bedrooms no one sleeps in.

- In recent years FEMA has only rarely provided trailer homes. Instead, FEMA usually helps a family to rent temporary lodging while their home is being repaired.

- Renters can get help for damaged personal property, such as furniture or appliances damaged by water or power surges, but fixing a rented dwelling is the sole responsibility of the landlord.

- Grants are only available for a person’s primary residence—rental property and second homes can only receive loans.

- Assistance is only provided to actual homeowners. He was surprised at how many people cannot prove they own the house they live in because they inherited the property or it is legally owned by a relative or ex-spouse. And sometimes proof of ownership gets lost in the disaster.

- FEMA does not help with mold that might develop as a result of a leaking roof or delayed repairs from flood damage. Homeowners need to fix these problems right away, weeks or months before financial assistance is awarded.

- Those who live in a flood zone and obtain assistance without signing up for the government flood insurance program won’t receive help the next time disaster strikes.

- FEMA’s Individual and Household Assistance program does not help those who are not legal citizens (unless a child is a citizen), or who were homeless at the time of the disaster.

Our source pointed out that the above list illustrates the complexity of FEMA’s assistance programs. In his experience, the application process was not easy for those who are unaccustomed to dealing with bureaucracy, particularly the elderly, chronically ill, mentally disabled, or anyone who has trouble comprehending government legalese. Letters often begin with, “You have been denied…”, which most people interpret as a stop sign instead of a speed bump that often can be overcome with an appeal letter (which needs to be notarized) and evidence of need. Many people who were dealing with the trauma of disaster or the stress of coping with its aftermath would simply give up on applying for FEMA aid, unaware that persistence pays.

Our informant explained that FEMA’s programs are extraordinarily complex as a result of the layered, piecemeal, inconsistent set of laws they are built upon. Regulations and procedures often seem more aimed at preventing duplication and fraud than assuring that every citizen who genuinely needs help gets it. Yet, his impression is that fraud is actually quite rare—he identified only two possible instances of attempted fraud out of the hundreds of applications he dealt with. FEMA’s complexity requires a huge and cumbersome bureaucracy to administer the programs; antiquated computer systems require a high degree of staff training, which the agency struggles to provide. He observed that FEMA employees who thoroughly understands the nuances of the various programs and who also possesses good customer service skills are rare.

Despite the agency’s flaws, our source says that FEMA does a lot of good work and he intends to continue with them. His major advice to homeowners and renters living on the vulnerable Eastern Shore is, “Obtain the best insurance policies you can afford. Don’t rely on FEMA or related organizations to make you whole.” Dangerous climate change is not a distant future threat, but today’s reality.

Common Sense for the Eastern Shore